When it comes to strategic planning for nonprofits, one of the key factors to consider is risk assessment. By understanding the potential risks and rewards associated with various actions, nonprofit leaders can make more informed decisions about where to allocate resources.

This article will discuss how risk assessment is used in strategic planning for nonprofits, as well as some of the next steps.

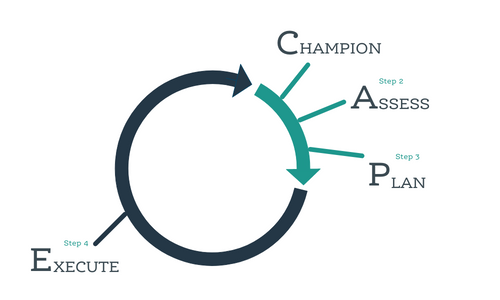

Strategic Planning and the CAPE Cycle

Nonprofit strategic planning is an essential tool for any organization looking to increase its effectiveness and make a lasting impact. It involves setting goals, developing strategies to achieve them, and creating systems for monitoring progress towards those objectives.

Strategic planning also helps organizations identify opportunities that can help them reach their desired outcomes more quickly or with greater success. By taking the time to create strategic plans, nonprofits can ensure they are making the most of their resources while achieving maximum results.

At Mission Met, we view strategic planning as a cyclical, never-ending, four-step process that we call the CAPE Cycle. As indicated in the graphic below, CAPE is an acronym for the four strategic planning steps: Champion, Assess, Plan, and Execute.

The second step of Mission Met’s strategic planning process is Assess.

The first and most obvious reason for the assessment step is to gather information about your organization and the environment in which it operates in order to create a relevant plan. Without that information then you’ll just be throwing darts in the dark.

The second and less obvious reason is that conducting an assessment serves as an excellent way to engage others and create buy-in for your strategy. There’s a saying that we use with our clients: “People support that which they help create.” You’ll learn more about the organization if all team members and key stakeholders provide input.

Assessing Risk in Your Nonprofit

Managing risk in your nonprofit can be a challenging but highly beneficial undertaking. Taking steps to properly assess and manage risk can help you anticipate and prepare for a variety of situations, allowing you to remain resilient regardless of what challenges may arise.

Risk agility also means that your organization is working efficiently while upholding its values and mission. This is essential in order to build trust with stakeholders and donors. Furthermore, engaging in holistic risk management can lead to more strategic decisions as well as increased cost savings down the line.

Risk assessment involves looking at both internal and external factors that may affect an organization’s operations or ability to achieve its goals. Internally, this includes analyzing financial statements in order to identify potential liabilities and areas of concern as well as evaluating staffing levels and organizational structure. Externally, risk assessment requires considering possible changes in the environment or legal landscape which could impact operations such as new regulations or changing donor preferences.

Assessments can be done in a variety of ways. You can assess risk and then make a plan by prioritizing how to respond to those risks. You can also assess strengths and opportunities.

A well-known analysis that assesses both is the SWOT analysis which finds the strengths, weaknesses, opportunities, and threats. Risk Alternatives offers a sophisticated four-step assessment process that identifies risks, both negative and positive, and helps determine how to address them.

What’s Included in a Risk Assessment?

We include topics and questions during an assessment that will capture where your organization is today and clarify your vision for the future (we typically suggest a vision for three years in the future). The action steps to get from where you are today to the three-year vision become part of your strategic plan.

First, capture key information about your organization’s programs, income, and people:

Include brief descriptions of all your services and programs and key metrics for those programs.

What is your estimated income for this year? What was it last year?

How many employees, contractors, board of directors, and volunteers do you have?

Next, review your organization’s processes and procedures for financials:

Do you have an annual budget? Do you have a multi-year budget?

Do your budgets set aside operating reserves?

Do you have a financial team or committee that regularly reviews your finances?

Do at least two people on your team have access to financial records and know how to create reports?

Do you have financial policies and procedures documented?

Does your board provide effective oversight of your financials?

You can also assess your organization’s current capacity in a variety of topics such as programs, board management, and fundraising. Additionally organizations may assess psychological risks including poor morale, stress or lack of motivation among team members.

A three-year vision will answer these types of questions:

What will your organization’s programs/services consist of?

How many staff members do you hope to have and what will their roles be?

What will your budget and expenses look like?

There are a number of ways you can conduct an assessment but these basics are a starting point.

Next Steps

After receiving responses from your assessment, analyze the threats and opportunities and determine the priorities for your organization. A consultant can help you pull out themes and prioritize the most urgent.

Often, themes will be abundantly clear. For example, if you have a new CEO, you may want to focus on the leadership transition. Or maybe you’ve recently been audited so we would recommend financial management as a priority.

After analyzing this information and identifying your themes, you can move to creating specific and measurable goals. This moves your team into Step 3 of the CAPE Cycle, the actual creation of your strategic plan.

Conclusion

Risk is an inevitable part of running a nonprofit organization. Being aware of potential risks and taking steps to minimize the negative and maximize the positive is key to protecting both your organization and your stakeholders while making the most impact in your community.

Through thoughtful planning and regular monitoring, you can face risks head on—and come out ahead!